If you own land in Florida and are even thinking about selling, the conversation around a 1031 exchange is unavoidable. It gets pitched as a powerful tax deferral strategy, and in the right context, it can be. But too often, landowners step into this process with incomplete information, misaligned expectations, and exposure they do not recognize until it is too late.

The Illusion of a Simple Tax Strategy

Many landowners enter into exchanges thinking they are executing a straightforward tax strategy, only to discover that the process is rigid, highly scrutinized, and unforgiving when mistakes are made.

The issue is not that 1031 exchanges are ineffective. The issue is that they are often approached without a full understanding of the compliance structure behind them. That gap creates unnecessary risk.

Intent Classification Is Not Optional

One of the most overlooked aspects of a 1031 exchange is how the IRS evaluates intent. Not all land automatically qualifies as investment property. If there are signs that the land was held for personal use, future residential plans, or inconsistent purposes, the exchange may not hold up under scrutiny.

Intent is not based on what is stated at closing. It is based on behavior over time. Holding period, marketing approach, and actual use all contribute to how the property is classified. Many Florida landowners assume vacant land qualifies by default. That assumption can lead directly to disqualification.

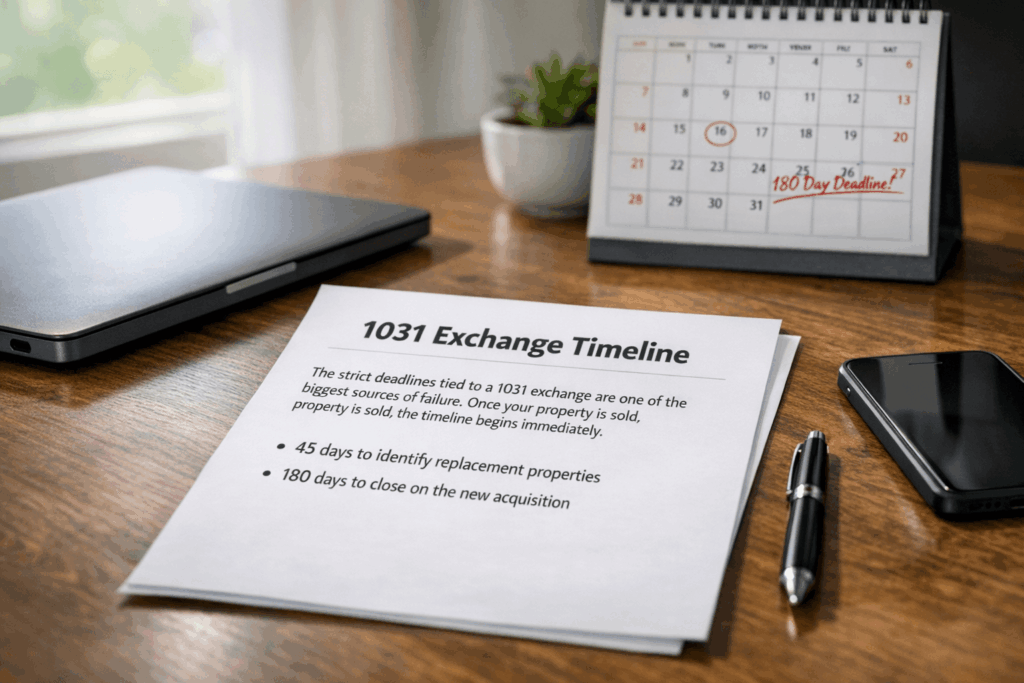

Timing Pressures Create Bad Decisions

The strict deadlines tied to a 1031 exchange are one of the biggest sources of failure. Once your property is sold, the timeline begins immediately.

- 45 days to identify replacement properties

- 180 days to close on the new acquisition

These deadlines do not adjust for market conditions or inventory shortages. In Florida, where land availability can vary significantly by region, this often forces investors into rushed acquisitions. Instead of selecting a strong asset, they select an available one. That shift in decision-making introduces long-term investment risk that outweighs the short-term tax benefit.

Intermediary Risk Is Often Ignored

A qualified intermediary is required to facilitate the exchange and hold the proceeds. This is a compliance necessity, but it also introduces a dependency that many investors underestimate. Errors in fund handling, documentation, or timing can collapse the exchange entirely.

Not all intermediaries operate at the same level of discipline. A failure at this stage does not result in a minor correction. It results in a full taxable event.

Financing Complications and Hidden Tax Exposure

When financing is involved in the replacement purchase, the structure must align with the value and equity of the property being sold. If it does not, the investor may trigger taxable gain through what is known as “boot.”

This is where many transactions begin to unravel. Investors focus on identifying a property but fail to structure the acquisition correctly. By the time the issue is identified, options are limited and costly.

Florida Land Comes With Its Own Risks

Not all land is equal, and Florida presents unique considerations that can materially affect your outcome. Zoning restrictions, environmental factors, access limitations, and development constraints all impact the usability and long-term value of a property.

When a 1031 exchange forces speed, due diligence often suffers. Investors become focused on completing the exchange rather than evaluating the quality of the replacement asset. That is a fundamental mistake. Tax deferral does not compensate for a poor acquisition.

Marketing Practices Are Adding to the Problem

There is a growing pattern in the land market where properties are positioned specifically to attract 1031 buyers. These listings often emphasize eligibility while downplaying limitations. The result is a cycle where sellers exit one questionable asset and enter another under the pressure of compliance deadlines.

This is not a strategic reinvestment. It is a continuation of risk.

Documentation Must Be Defensible

A valid 1031 exchange requires more than meeting deadlines. It requires a clear, consistent, and well-documented investment intent. Any inconsistencies between how the property was used, marketed, or described can be used to challenge the legitimacy of the transaction.

This is where many investors fall short. Documentation is treated as a formality instead of a critical control point.

Not Every Sale Should Lead to an Exchange

There is a strong assumption in the market that deferring taxes is always the best move. That is not always true. In some cases, recognizing the gain and resetting your investment position may provide more flexibility and less long-term risk.

If suitable replacement properties are not available, forcing a 1031 exchange can do more harm than good. The decision should be based on overall investment strategy, not just tax avoidance.

Summary

Landowners are entering 1031 exchanges without fully understanding the constraints, timelines, and documentation standards required to keep the transaction compliant. This leads to rushed acquisitions, weakened asset quality, and avoidable tax exposure. Land By Owner prioritizes disciplined execution, clear investment intent, and defensible transaction structure. Whether exiting or reinvesting, the focus remains on reducing regulatory gray areas and aligning every decision with a legitimate business-purpose strategy.