The distinction between mobile homes and modular homes is frequently blurred in marketing, sales positioning, and transaction structuring. This lack of clarity creates material risk for buyers, sellers, and operators, particularly when asset classification directly impacts financing eligibility, titling, regulatory oversight, and long-term value expectations.

1. Classification Differences: Structural and Regulatory Misalignment

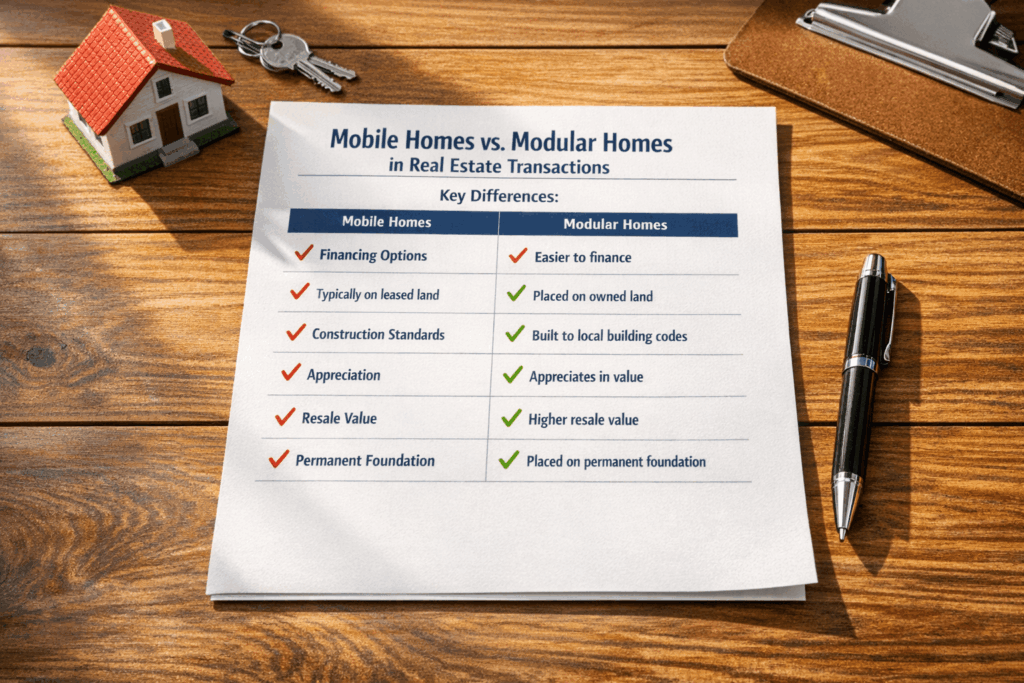

Mobile homes (commonly referred to as manufactured housing) and modular homes are fundamentally different asset classes, yet they are often presented interchangeably in listings and promotional materials.

Mobile homes:

- Are built to federal HUD standards

- Are typically titled as personal property unless converted

- May be located in leased land communities

- Are often subject to different financing frameworks

Modular homes:

- Are built to state and local building codes

- Are permanently affixed to real property

- Are generally titled as real estate

- Follow traditional residential construction standards

Failure to clearly distinguish these classifications introduces risk of misrepresentation, particularly when buyers assume real property characteristics that do not legally apply.

2. Financing Implications: Consumer Credit Exposure

The classification of the structure directly affects financing pathways. Mobile homes are frequently financed through chattel loans or personal property lending structures, while modular homes typically qualify for traditional mortgage products.

Mislabeling or loosely describing a mobile home as “modular” or “similar to site-built housing” may:

- Lead buyers to expect conventional mortgage eligibility

- Create confusion regarding collateral classification

- Trigger compliance concerns under consumer credit regulations

Where financing expectations are not aligned with the true asset classification, the transaction may result in borrower dissatisfaction, failed closings, or regulatory scrutiny.

3. Titling and Ownership: Documentation Risk

Mobile homes and modular homes follow different titling processes, which must be accurately disclosed and documented.

Mobile homes:

- Often retain a vehicle-style title unless legally converted

- May require title retirement to be classified as real property

Modular homes:

- Are deeded as part of the real estate from inception

Failure to properly disclose titling status or conversion requirements can result in:

- Clouded ownership records

- Delays in transfer or resale

- Legal disputes regarding property classification

This represents a documentation integrity issue that cannot be resolved through marketing disclaimers alone.

4. Valuation and Market Positioning: Misleading Comparisons

Marketing materials frequently position mobile homes alongside modular or site-built homes in a way that implies equivalent value, durability, or appreciation potential.

This creates a risk where:

- Buyers overestimate long-term value retention

- Sellers rely on unsupported pricing comparisons

- Appraisal expectations become misaligned with asset reality

Mobile homes, particularly those not converted to real property, may depreciate differently than modular or site-built homes. Failure to clearly communicate this distinction undermines transaction transparency.

5. Land Use and Ownership: Structural Dependency Risk

A critical distinction lies in the relationship between the structure and the land.

Mobile homes:

- May be located on leased land

- Are not inherently tied to land ownership

Modular homes:

- Are permanently affixed to owned land

- Function as integrated real property improvements

When this distinction is not clearly disclosed, buyers may incorrectly assume they are acquiring both land and structure under traditional real estate norms. This misunderstanding introduces significant risk in both acquisition and long-term occupancy planning.

Summary

The continued conflation of mobile homes and modular homes in real estate transactions reflects a broader issue of classification ambiguity and inconsistent disclosure practices.

Without stricter differentiation, standardized disclosure practices, and reinforced documentation controls, these transactions remain vulnerable to consumer confusion, failed expectations, and regulatory scrutiny.

For Land By Owner, maintaining clear and consistent asset classification across marketing, documentation, and transaction structure is essential to reduce ambiguity and support defensible, business-purpose positioning.

Clear classification is not a marketing preference, it is a compliance requirement, and a necessary foundation for maintaining transaction integrity.