Florida’s real estate environment is entering a phase of measured stabilization following multiple years of volatility tied to rate increases, insurance cost expansion, and accelerated pricing cycles. Current conditions reflect normalization across several regions, with inventory growth and moderated pricing contributing to a more structured and data-driven acquisition environment.

For business-purpose operators, 2026 reflects a transition from reactive positioning to disciplined market selection and long-term portfolio alignment.

Capital Environment and Cost of Funds

The broader capital environment is expected to stabilize, with borrowing costs showing reduced volatility compared to prior years. While rates remain elevated relative to historical lows, improved predictability supports underwriting consistency and acquisition modeling.

Stable financing conditions influence:

- acquisition pacing

- construction pipeline decisions

- refinance timing strategies

The emphasis shifts from rate timing to deal structure and risk-adjusted entry.

Pricing Behavior and Affordability Adjustments

Price growth across Florida has moderated following the accelerated expansion period of 2020 through 2022. This adjustment phase reflects:

- reduced speculative pressure

- recalibration of seller expectations

- increased sensitivity to carrying costs, including insurance and taxes

From a business-purpose perspective, this creates a more analyzable pricing environment rather than a rapid appreciation cycle.

Key contributing factors include:

- stabilization in borrowing costs

- slower price appreciation

- income growth in select employment sectors

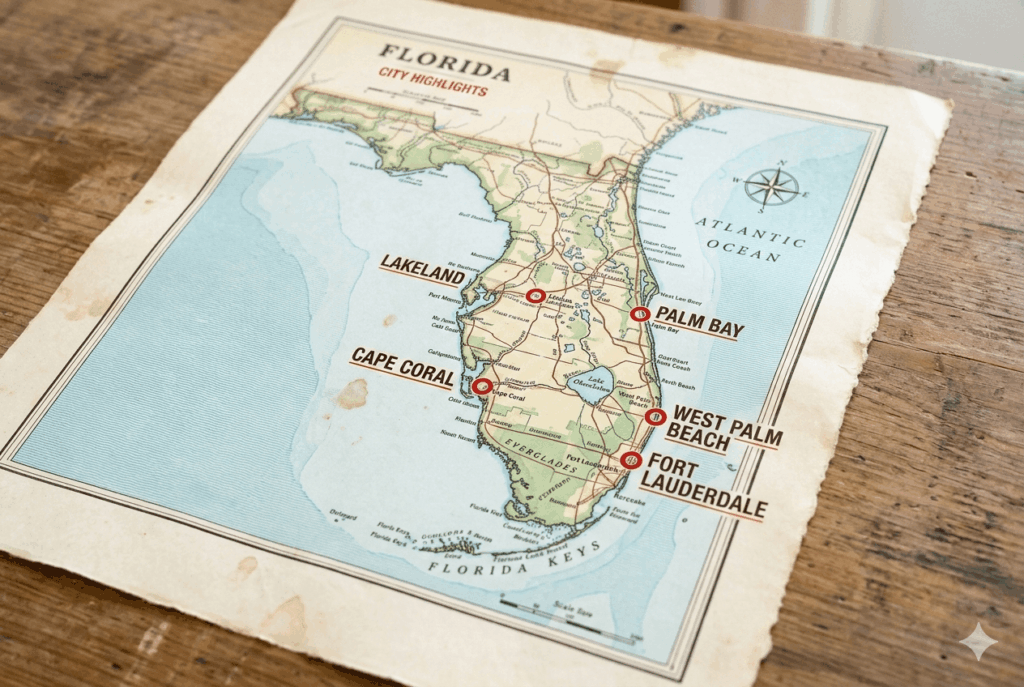

Regional Market Corrections and Segmentation

Market behavior is not uniform across Florida. Certain regions are experiencing downward price adjustments driven by cost pressures and prior overextension.

Notable areas of correction include:

- Cape Coral

- Fort Lauderdale

- Lakeland

- Palm Bay

- West Palm Beach

These adjustments reflect normalization rather than systemic weakness. Increased transaction activity in some counties indicates price discovery is occurring, and liquidity is returning under revised expectations.

For operators, this reinforces the importance of submarket analysis rather than statewide assumptions.

Inventory Expansion and Supply Rebalancing

Inventory levels are increasing due to a combination of new construction completions and existing owners entering the market. This shift reduces the supply constraints seen in prior years.

Implications include:

- expanded acquisition options

- reduced competitive bidding pressure

- improved ability to negotiate pricing and terms

- more accurate valuation alignment

A more balanced supply-demand relationship supports disciplined underwriting and reduces reliance on accelerated appreciation assumptions.

Long-Term Demand Drivers

Florida continues to experience sustained population inflows driven by economic migration, tax structure, and business relocation trends. These factors contribute to long-term demand across multiple real estate segments.

Demand drivers relevant to business-purpose strategies include:

- continued in-migration

- employment growth in key sectors

- expansion of rental demand

- development of secondary and tertiary markets

While short-term fluctuations exist, long-term structural demand remains intact through the end of the decade.

Transaction Volume Outlook

Industry projections indicate a potential increase in transaction activity as market conditions stabilize. Increased volume is primarily tied to:

- improved pricing alignment

- expanded inventory availability

- reduced uncertainty in financing conditions

This should be interpreted as a normalization of transaction flow rather than an acceleration phase.

Operational Considerations for Market Participants

Acquisition Strategy

- prioritize submarket-level data over statewide trends

- underwrite conservatively with insurance and tax sensitivity

- focus on basis rather than projected appreciation

Disposition Strategy

- align pricing with current comparable activity

- account for longer exposure times in certain markets

- avoid reliance on prior peak valuations

Portfolio Management

- monitor holding costs closely

- evaluate geographic risk concentration

- adjust asset mix based on demand stability

Florida’s 2026 real estate environment reflects stabilization, localized corrections, and sustained long-term demand fundamentals. Market conditions support disciplined acquisition and portfolio management rather than speculative positioning.

The current cycle favors operators who prioritize data-driven decisions, cost control, and market segmentation awareness.

Conclusion

At Land By Owner, the focus remains on maintaining clear business-purpose positioning across all transactions. Market stabilization reinforces the importance of structured acquisitions, documented investment intent, and disciplined underwriting.

As conditions normalize, reducing ambiguity in deal purpose, marketing language, and borrower profile becomes critical to maintaining compliance integrity and minimizing regulatory exposure.