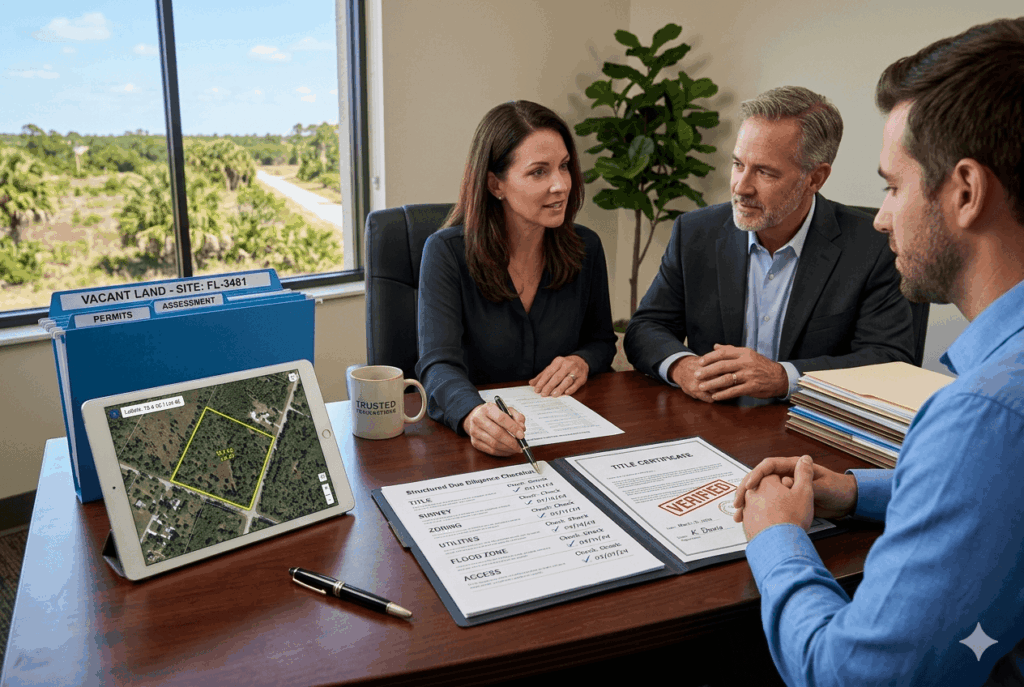

When a land buyer is approaching closing, the risk profile shifts from exploration to execution. At this stage, incomplete verification is one of the most common sources of post-closing disputes, regulatory exposure, and borrower dissatisfaction. A disciplined, documented due diligence process is not optional, it is essential for both transaction integrity and defensibility.

Below is a structured checklist designed to eliminate ambiguity and ensure the transaction aligns with business-purpose intent, avoids consumer credit misclassification risk, and withstands scrutiny.

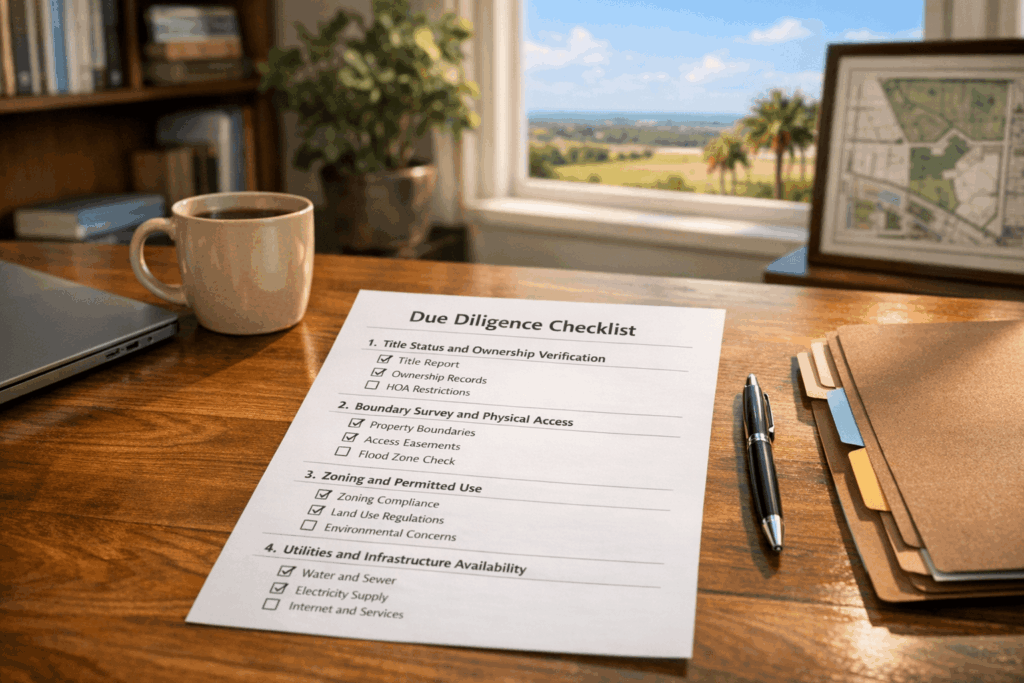

1. Title Status and Ownership Verification

Before closing, confirm that title is clear, marketable, and insurable. This includes:

- Reviewing the title commitment for liens, judgments, or encumbrances

- Verifying the legal description matches marketing and contract documents

- Identifying easements, restrictions, or rights-of-way that may impair use

Any unresolved title defect introduces downstream servicing risk and potential enforcement issues. If seller financing is involved, unclear title can impair lien priority and collateral enforceability.

2. Boundary Survey and Physical Access

A current survey is critical, not a legacy or assumed boundary.

- Confirm property boundaries align with legal description

- Identify encroachments, overlaps, or access limitations

- Verify ingress/egress is legally recorded, not implied

Lack of legal access is one of the most common, and most damaging, failures in land transactions. “Physical access” (a visible path) is not the same as legal access. From a compliance standpoint, marketing land without verified legal access creates misrepresentation exposure.

3. Zoning and Permitted Use

Zoning must be verified directly with the county or municipality not inferred.

- Confirm zoning classification (e.g., agricultural, residential, mixed-use)

- Validate intended use is permitted under current regulations

- Check for future land use changes or pending zoning amendments

Misalignment between buyer intent and zoning creates both reputational and regulatory risk. If financing is extended, and the borrower cannot use the property as represented, this may raise consumer protection concerns, especially if the buyer is unsophisticated.

4. Utilities and Infrastructure Availability

Do not rely on generalized statements like “utilities nearby.”

- Confirm availability of electricity, water, and sewer (or septic feasibility)

- Identify connection costs, distance to tie-in points, and permitting requirements

- Verify road maintenance responsibility (county vs private)

Utility assumptions are a frequent source of borrower complaints. From a marketing compliance standpoint, all utility representations must be precise, supportable, and documented.

5. Flood Zone and Environmental Constraints

Flood risk directly impacts usability, insurance costs, and financing viability.

- Review FEMA flood zone maps

- Determine if the property lies within a Special Flood Hazard Area (SFHA)

- Assess wetlands, protected species, or environmental restrictions

Failure to disclose material environmental limitations can create significant liability. Additionally, if a property is effectively unusable without substantial mitigation, the transaction may not meet reasonable business-purpose standards.

6. Access to Financing vs Consumer Credit Risk

If the transaction involves seller financing or structured payments, classification matters.

- Confirm the purchase is for business or investment purpose, not personal use

- Document borrower intent clearly and consistently across all materials

- Avoid marketing language that implies residential or consumer use if not applicable

Improper classification can trigger regulatory exposure under federal consumer credit frameworks. Transactions that appear consumer-oriented but are structured as business-purpose create audit vulnerability.

7. Property Taxes and Assessments

Outstanding taxes or special assessments must be identified and addressed.

- Verify current tax status and payment history

- Identify any pending reassessments or improvement district fees

- Confirm prorations at closing are accurate

Unexpected tax liabilities can impair borrower performance and increase servicing friction. From a portfolio standpoint, tax delinquency risk must be minimized upfront.

8. Restrictions, Covenants, and HOA Impacts

Deed restrictions and community rules can significantly limit use.

- Review Covenants, Conditions, and Restrictions (CC&Rs)

- Identify HOA requirements, dues, and enforcement mechanisms

- Confirm restrictions do not conflict with buyer’s intended use

Non-compliance with restrictions can result in fines, legal action, or forced remediation—creating avoidable borrower distress.

9. Documentation Consistency and Marketing Alignment

All representations made during marketing must align with actual property characteristics.

- Ensure listings, ads, and sales communications are accurate and supportable

- Avoid exaggerated or implied claims (e.g., “build-ready” without verification)

- Maintain a record of all disclosures provided to the buyer

This is a key area of regulatory exposure. Inconsistent or misleading marketing—especially in land transactions—can be construed as deceptive practice.

10. Closing Documentation and Audit Trail

Every due diligence step must be documented.

- Retain title reports, surveys, zoning confirmations, and utility verifications

- Ensure buyer acknowledgments are signed and complete

- Maintain a defensible audit trail for the full transaction lifecycle

If a transaction is ever reviewed, internally or externally, documentation is the primary line of defense. “Assumed verification” is not defensible.

Final Risk Perspective

A land transaction is only as strong as its weakest verification point. For buyers near closing, the focus should shift from opportunity to validation. For operators, especially platforms like Land By Owner, the obligation extends further: ensuring that every listing, representation, and financing structure is aligned with verified facts and business-purpose intent.

Failure to enforce disciplined due diligence standards introduces layered risk misrepresentation exposure, consumer credit misclassification, and long-term servicing instability. A consistent, checklist-driven process is not just operational best practice; it is a necessary control to protect portfolio performance and regulatory positioning.

Anything less introduces avoidable risk.